By Syed Aoon Sherazi

Walk through the gates of Pakistan Steel Mills today and you won’t hear a single furnace running. The plant has been silent since 2015. And yet, somehow, its books keep getting heavier. The debt climbs. The liabilities pile up. The loans keep flowing in from Islamabad. There’s even a small but steady stream of theft cases from a site that, on paper, has nothing left to steal. It’s a strange kind of afterlife for a company that stopped making steel a decade ago, still very much alive on the balance sheet, even though the production line died years back.

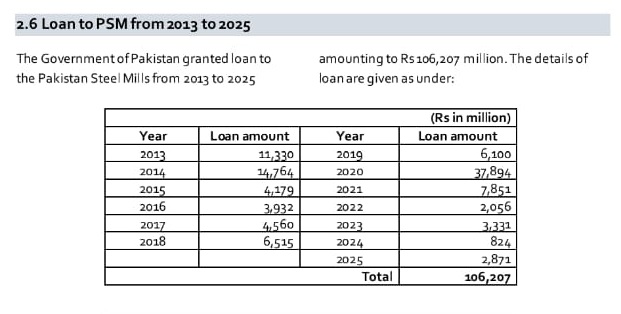

None of this happened in isolation. On top of the collapsing revenue and the growing liabilities, the federal government has quietly loaned PSM Rs 106,207 million between 2013 and 2025, just to keep the lights nominally on. It broke down like this: Rs 11,330 million in 2013, Rs 14,764 million in 2014, Rs 4,179 million in 2015, Rs 3,932 million in 2016, Rs 4,560 million in 2017, Rs 6,515 million in 2018, Rs 6,100 million in 2019, a huge Rs 37,894 million in 2020, Rs 7,851 million in 2021, Rs 2,056 million in 2022, Rs 3,331 million in 2023, Rs 824 million in 2024, and Rs 2,871 million in 2025. That single 2020 figure is worth sitting with for a second Rs 37.9 billion, more than a third of everything loaned across thirteen years, handed over five full years after the plant had already gone dark. Not a rescue. Not an investment. Just the cost of keeping a corpse on a ventilator.

What follows is the anatomy of exactly what that money has been keeping alive.

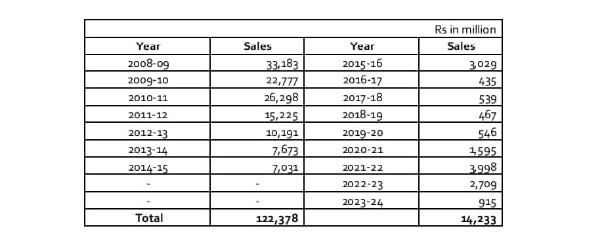

Go back to the last stretch when PSM was actually functioning FY2008-09 through FY2014-15 and the company brought in Rs 122,381 million in revenue. That’s a mill doing its job: making steel, selling steel. Fast forward to the nine years since the 2015 shutdown, and total revenue comes to just Rs 14,236 million. That’s roughly a tenth of what it used to bring in, and it isn’t even real production revenue, it’s money from selling off leftover inventory sitting in the warehouse: billets, slabs, blast furnace material, coal tar, whatever scraps of the old operation could still find a buyer. For nine years, PSM hasn’t been running a business so much as slowly selling off its own remains.

Then there’s the trade debt problem, and this one is genuinely hard to explain away. In FY2023, PSM was owed Rs 523 million by customers and other parties. A year later, in FY2024, that number had exploded to Rs 17,600 million a 236% jump. You’d expect a company watching its receivables balloon like that to also revise how much of it they actually expect to collect. PSM didn’t. The provision set aside for doubtful debts sat frozen at Rs 3,500 million the whole time. So a receivables book that grew more than thirtyfold wasn’t matched by even a slightly more cautious view of collectability, which is the kind of thing that makes auditors, and honestly anyone reading these numbers, raise an eyebrow.

Liabilities tell a similar story. Back in FY2016-17, PSM owed Rs 177,411 million. By FY2023-24, that figure had swelled to Rs 357,985 million more than double, accumulated during years when the plant wasn’t producing anything to help pay it down. With no operating revenue coming in, PSM’s ability to meet its obligations rests almost entirely on the government continuing to bail it out. And here’s the uncomfortable part: on paper, PSM’s balance sheet still looks impressive. thousands of acres of land, plant and machinery, warehouses of inventory. But almost none of it can actually be turned into cash right now. These are dead assets. A “strong” balance sheet doesn’t mean much if nothing on it can generate a rupee of operating income without a restructuring or a sale first.

Even the small stuff hasn’t been managed well. Buried in PSM’s unresolved receivables is a batch of unpaid dues from schools and colleges sitting inside Steel Town, the company’s own residential township. Madar-e-Millat Degree College,owes just over Rs 2 million. Allama Iqbal Girls Secondary School, owes over Rs 7.1 million. Shah Lateef Boys Secondary School owes just over Rs 6 million. Madar-e-Millat College of Education, Chakar Khan Primary School, Sir Syed Primary School, Aghosh Special Children School and College, and the Institute of Computer Science round out the list. Add it all up 3,364 students across eight institutions and PSM has failed to recover Rs 19,454,519. It’s a rounding error next to the billion-rupee losses elsewhere, but it says something: if a state-owned company can’t even collect school fees from institutions on its own property, it’s hard to trust it with the bigger numbers.

And then there’s the theft. A plant that hasn’t made steel in almost ten years is still, somehow, getting robbed. Copper bus bar disappeared from MSGR on 11 July 2024. Cable went missing from the PDN store on 3 August 2024. Around 550 feet of PDN cable vanished from various locations around the site. Copper material was stolen from the Gharo Pumping Circle, part of the Bulk Water Supply Distribution Network. Cable and bus bar were taken from MMGDC College in Steel Town in late October 2024. The Purchase Department was hit in March 2025, and MMGDC College again in May 2025. All told, these incidents add up to Rs 9.597 million and as far as anyone can tell, none of the investigations have actually been closed out. It’s a small but telling detail: even with production dead, there’s apparently still enough unguarded copper and cable lying around to make theft worthwhile, and not enough oversight to stop it.

Put it all together the losses, the debt, the liabilities the Board is now on the hook for and you get a figure of Rs 445,948 million. That’s the scale of the hole. It’s now the current Board’s job to get a handle on it: finalize accounts properly, deal with people illegally occupying residential units, crack down on theft and mismanaged assets, and actually go count what the company still owns instead of assuming the books are right.

Line the loan history up against everything else in this report, and the pattern gets hard to ignore: revenue down roughly 90% since 2015, liabilities nearly doubled since the shutdown, receivables growing in ways nobody seems willing to scrutinize and government loans, instead of tapering off as you’d expect from a company being wound down, actually spiking to their highest point in 2020, five full years after the plant went dark.

None of these numbers are hidden or disputed they come straight from the government’s own Audit Report, the same report that’s now openly calling this situation unsustainable. The Audit Report doesn’t mince words about what needs to happen: turn the idle land, plant, and equipment into something that actually earns money, whether through privatization, leasing, or bringing in a private partner. Tie any further government support to an actual restructuring plan, not another open-ended check. Get the day to day cash problems under control without leaning on more loans, and start enforcing the basics chase down the unpaid dues, deal with the theft, stop the unauthorized occupation of company housing. Any further layoffs need to be handled carefully, in line with labour law, not as another improvised cost-cutting move. And the Audit Report is blunt about the bottom line: there is no third option here. Either PSM actually gets revived as a working business, or its assets get sold. Everything in between is just a slower, more expensive version of decline.

That, ultimately, is what the Audit Report leaves you with a company whose revenue has fallen by roughly 90%, whose liabilities have nearly doubled since it stopped producing, whose receivables have grown without anyone adjusting for the risk, and whose own compound still can’t keep copper wire from walking off the premises. Add in more than Rs 106 billion in government loans just to hold this position in place, and you start to see why the Audit Report keeps returning to the same warning: PSM’s assets on paper mean very little without a real revenue stream behind them. Until a revival plan or a sale actually happens not just gets proposed, every year that passes without one just widens the gap between what the mill owes and what it can produce, funded by loans that look less like a bridge to recovery and more like the price of putting off a decision no one wants to make.